Today is the day. Hours of meetings. Plenty of emails. Last-minute hesitation that you artfully overcame. Today is the day that you sign the contract.

In the sales process, we spend an untold number of hours and dollars on optimizing the funnel, customizing marketing material, and honing the pitch. But by the time we get to the ‘Yes,’ how much effort do we put into the contract? Sure, lots of effort, but that’s legal’s job, right? Maybe we give it a cursory review before sending it over to the customer, but by the time the deal is about to close, we are ready to pop the champagne, not pop open the contract.

There are always a few who prove the rule - I have known quite a few insurance agents that read every couple hundred-page policy before sending it for signature. Though this is not the norm.

Already difficult to understand, policy documents make for great nighttime reading. Which is fine until there is a claim. To improve clarity, consumer understanding, and legal defensibility, some insurers are adopting ‘smart contracts,’ a way to increase value and transparency for insurers, brokers, and insureds.

Putting the smarts in contracts

Blockchain technology is a transactions ledger built on a shared database filled with entries that other entities contributing to the blockchain (called peer-to-peer networks) must confirm. It is helpful to envision it as a strongly encrypted and verified shared Google Document, in which each entry in the sheet depends on an immutable (or unchangeable) relationship to all its predecessors. Before it can save the new entry, everyone in the network must agree that it is valid.

Check out this article where we break down other innovative blockchain uses

Smart contracts work by following simple “if/when… then…” statements that are written into code on a blockchain. A network of computers executes the actions when predetermined conditions have been met and verified. These actions could include releasing funds to the appropriate parties, registering a vehicle, sending notifications, or issuing a ticket. The blockchain is then updated when the transaction is completed. That means the transaction cannot be changed, and only parties who have been granted permission can see the results.

Within a smart contract, there can be as many stipulations as needed to ensure the contract is accurately codified. To establish the terms, participants must determine how transactions and their data are represented on the blockchain, agree on the “if/when...then…” rules that govern those transactions, explore all exceptions, and define a framework for resolving disputes.

The Benefits of Smart Contracts

Smart contracts require fewer intermediaries and fewer touchpoints across the journey from quote to bind to claims administration. Fewer steps directly translate to lower administrative costs for everyone involved and increases transparency. As a result, smart contracts can enable insurers to lower premiums and improve commissions.

The impact on customer onboarding

As regulations continue to grow around the reliability and integrity of data, customer onboarding is an area where smart contracts can create efficiencies. Imagine a client wants a new policy. With blockchain technology, all this client would have to do is give you access to a link to encrypted data, which will save you time and money as you will not have to chase down those details.

Since the data exists on a blockchain, other network members have verified it, confirming its integrity. Perhaps more importantly, in this era when an increasing number of customers want their information to remain private, blockchain puts the customer firmly in the driver’s seat by giving them the power to grant (and revoke) permission to those with whom they want to share their information. This provides the peace of mind of knowing one’s information is safe and cannot be tampered with.

In the past 18 months, a few existing blockchain consortiums have created a working distributed ledger infrastructure for identity management that interested organizations can join. For instance, over 70 organizations, including financial firms, law firms, tech, and cybersecurity companies, have joined The Sovrin Network since it went live in September 2017.

Underwriting applications

Today’s underwriters review applications and evaluate risks. This process will be simplified and faster by offering the insurance policy as a smart contract. It creates an understanding of the applicable conditions and becomes the foundation for automated claims processing.

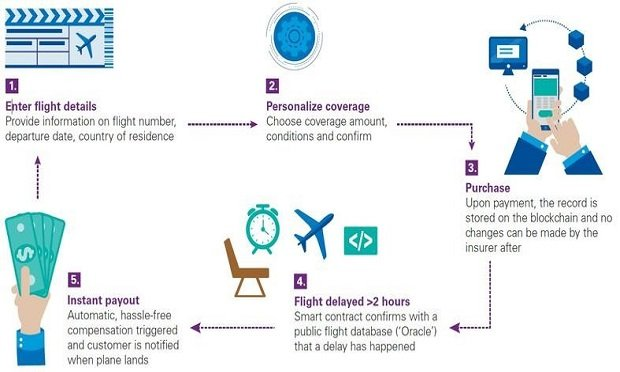

Fizzy, for example, is an automated parametric flight delay insurance platform launched by AXA in 2017. It records information on policyholders’ delayed flight insurance using smart contracts and connects to global air traffic controller databases, then checks on the status of the flights. If a policyholder experiences a delay of two or more hours, as reported by the airport, the smart contract automatically triggers the mechanism for paying the insured upon the receipt of flight confirmation by the policyholder.

Efficient claims processing

The evaluation and processing of P&C claims are complex. It involves data from various systems and requires a lot of coordination among stakeholders. A smart contract — which is built on blockchain technology and intended to eliminate third parties — is an excellent way to manage the process and create efficiencies.

Consider an insurance company with a smart contract in place for a policyholder who has just been in a car accident. The carrier can quickly gather data from several external and internal sources to determine whether we should pay a claim. The insurer also can rapidly check many other data points such as smart devices in the car, weather reports, the driver’s records, police filings, and so on. This is all done automatically when the claim is submitted to the system.

Halos Insurance provides another example. This company leverages blockchain technology to enable self-service claim reporting for its policyholders. If a homeowner sees a damaged roof after a storm, the individual can use the Halos Dobby app to upload pictures for insurers and roofers.

Managing risk and minimizing fraud

Insurance fraud is on the rise, which is costly for insurers and insureds. Part of the expense comes from a paperwork-intensive claims process. This antiquated process allows criminals to easily make multiple claims to different insurers for a single loss or split the claims and over-represent the damage.

Currently, insurers integrate data with various other public sources to prevent fraud, and this data is leveraged to identify fraud patterns. By adding in blockchain, however, there would be broader access that would allow for better profiling of the transactions to identify bad behavior.

Helping to build the future

For smart contracts to become truly ubiquitous in insurance, carriers will have to adopt them. But that does not mean that agents, brokers, and wholesalers do not have a role to play in the adoption of this technology. All insurance professionals can help persuade and influence insurers to pursue this technology. Doing so, we increase the speed at which policies can be underwritten and issued, putting more money in the pocket of agents and brokers.